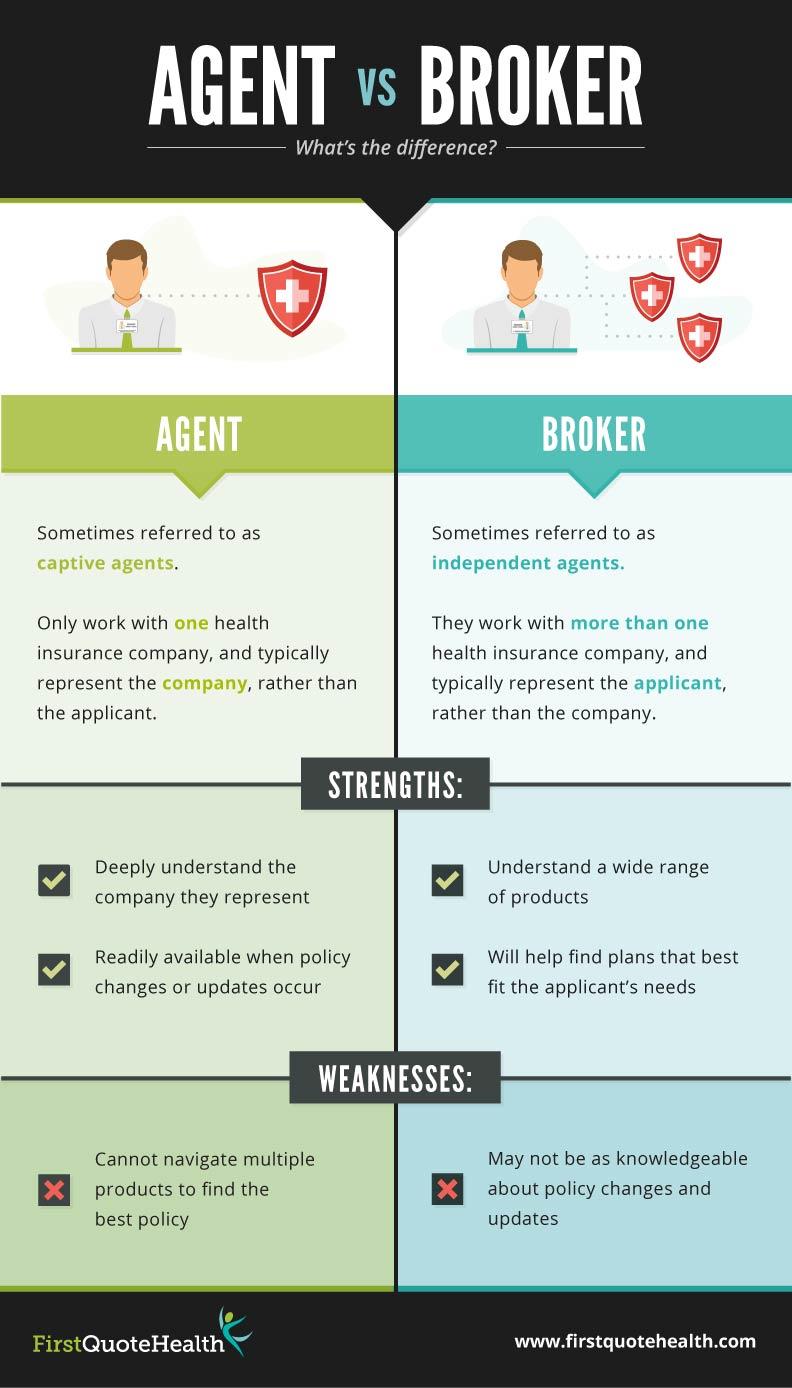

It is easy to get a Minnesota real estate license if you just follow these steps. These are the requirements to obtain a real estate license in Minnesota, including the pre-licensing education required, the real property examination and the cost. We also include helpful resources like the StateRequirementguide. Learn more. These are some tips to help make the process smoother. After you've read through the guides, you should be able to pass the exam on your first attempt.

Pre-licensing education

Minnesota real estate licenses require that you have completed at least 30 hours of training before becoming licensed. Pearson offers a real-estate course that can help you do this. This course provides a real estate dictionary, as well eBooks. Pearson VUE will allow you to apply to your license if you have successfully completed your prelicensing training. You'll need an account to apply.

Two forms of identification are required to pass the real estate exam. Your primary ID must be issued by the government and include your signature and picture. An additional ID must be valid, with the exact same details. Additional expenses may arise during the course. However, you can apply for your license at the Minnesota Commercial Division office, where you can get guidance and receive a diploma. You will need the broker or standard salesperson license if you plan to sell commercial real property in Minnesota.

Exam requirements

Before pursuing a career in real estate, it's important to understand the requirements and exam process. The process of granting permission for a person to practice real estate is called a license. Exams help ensure that they meet certain standards. It serves to protect the public by ensuring that anyone who practices real estate has the necessary qualifications and competence. Pearson VUE, an internationally recognized provider of assessment services, administers Minnesota's real-estate licensing examination program.

The national and state sections of the real estate licensing examination must be passed in order to obtain your license. The state-approved testing center administers the exams. They are divided into two sections: the national and state portions. You will be found guilty of gross misdemeanor if you fail the exam. You can't work as a broker or real estate agent until you have the license.

Requirements in order to renew

To ensure your license is up-to-date you will need to complete continuing education courses. You can take advantage the many opportunities for continuing education, whether you're in the middle of a transaction or at the beginning of your renewal process. Minnesota requires that you take at least one continuing education class every two years. However, you don't have to take more. Your courses should last at least 90 minutes. You can make it easier to meet the renewal requirements of your Minnesota real-estate license by taking at least 15 hours each year of continuing education.

You must also complete at least 22.5 hours in approved continuing education courses. You should also take at least one continuing education course in real estate law, rules and court cases. Courses should be at least an hour long and cover fair housing laws and agency laws. A training course that is specifically tailored for agents, brokers, or real estate agents can help you earn continuing education credits.

Cost

Pre-licensing education must be completed for 90 hours before you can become a Minnesota licensed real estate agent. Both online and classroom courses are acceptable. On-demand courses can be the most economical. You can expect to pay between $200-$300 for stand-alone courses. Minnesota license applicants must present two forms identification. You must have a valid government-issued ID with a photo and signature. Also, a second ID must be valid. It must have a photo of the applicant and a signature. Additional fees may be required for the pre-licensing education.

Minnesota's application fee includes a technology surcharge as well as a fund for real estate education and research. The application fee is not refundable if the application is incomplete. The $110 application fee can be paid by credit card. A minimum income of $50,000 and at least three years' experience in the real estate industry are required to qualify for a real-estate license. Minnesota requires that at least eighteen be present. You must hold a bachelor's level degree or have at least two years of college.

FAQ

How long does it usually take to get your mortgage approved?

It is dependent on many factors, such as your credit score and income level. Generally speaking, it takes around 30 days to get a mortgage approved.

How can I get rid of termites & other pests?

Your home will eventually be destroyed by termites or other pests. They can cause severe damage to wooden structures, such as decks and furniture. A professional pest control company should be hired to inspect your house regularly to prevent this.

Should I rent or own a condo?

Renting might be an option if your condo is only for a brief period. Renting will allow you to avoid the monthly maintenance fees and other charges. A condo purchase gives you full ownership of the unit. The space can be used as you wish.

Is it possible to sell a house fast?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. You should be aware of some things before you make this move. First, you must find a buyer and make a contract. You must prepare your home for sale. Third, advertise your property. Lastly, you must accept any offers you receive.

What should you think about when investing in real property?

You must first ensure you have enough funds to invest in property. You will need to borrow money from a bank if you don’t have enough cash. It is also important to ensure that you do not get into debt. You may find yourself in defaulting on your loan.

You also need to make sure that you know how much you can spend on an investment property each month. This amount must cover all expenses related to owning the property, including mortgage payments, taxes, insurance, and maintenance costs.

Also, make sure that you have a safe area to invest in property. It would be best to look at properties while you are away.

What are the advantages of a fixed rate mortgage?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This guarantees that your interest rate will not rise. Fixed-rate loans also come with lower payments because they're locked in for a set term.

What is a Reverse Mortgage?

Reverse mortgages are a way to borrow funds from your home, without having any equity. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers repayments.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to Manage a Rent Property

Renting your home can be a great way to make extra money, but there's a lot to think about before you start. We'll show you what to consider when deciding whether to rent your home and give you tips on managing a rental property.

Here are the basics to help you start thinking about renting out a home.

-

What factors should I first consider? You need to assess your finances before renting out your home. You may not be financially able to rent out your house to someone else if you have credit card debts or mortgage payments. It is also important to review your budget. If you don't have enough money for your monthly expenses (rental, utilities, and insurance), it may be worth looking into your options. It might not be worth the effort.

-

How much does it cost to rent my home? Many factors go into calculating the amount you could charge for letting your home. These factors include the location, size and condition of your home, as well as season. Remember that prices can vary depending on where your live so you shouldn't expect to receive the same rate anywhere. The average market price for renting a one-bedroom flat in London is PS1,400 per month, according to Rightmove. This means that if you rent out your entire home, you'd earn around PS2,800 a year. This is a good amount, but you might make significantly less if you let only a portion of your home.

-

Is this worth it? You should always take risks when doing something new. But, if it increases your income, why not try it? It is important to understand your rights and responsibilities before signing anything. Renting your home won't just mean spending more time away from your family; you'll also need to keep up with maintenance costs, pay for repairs and keep the place clean. You should make sure that you have thoroughly considered all aspects before you sign on!

-

Are there any advantages? You now know the costs of renting out your house and feel confident in its value. Now, think about the benefits. There are plenty of reasons to rent out your home: you could use the money to pay off debt, invest in a holiday, save for a rainy day, or simply enjoy having a break from your everyday life. You will likely find it more enjoyable than working every day. You could make renting a part-time job if you plan ahead.

-

How can I find tenants After you have made the decision to rent your property out, you need to market it properly. Online listing sites such as Rightmove, Zoopla, and Zoopla are good options. Once you receive contact from potential tenants, it's time to set up an interview. This will help you assess their suitability and ensure they're financially stable enough to move into your home.

-

How can I make sure I'm covered? If you fear that your home will be left empty, you need to ensure your home is protected against theft, damage, or fire. You'll need to insure your home, which you can do either through your landlord or directly with an insurer. Your landlord will usually require you to add them as additional insured, which means they'll cover damages caused to your property when you're present. If you are not registered with UK insurers or if your landlord lives abroad, however, this does not apply. In these cases, you'll need an international insurer to register.

-

Sometimes it can feel as though you don’t have the money to spend all day looking at tenants, especially if there are no other jobs. Your property should be advertised with professionalism. Make sure you have a professional looking website. Also, make sure to post your ads online. Additionally, you'll need to fill out an application and provide references. Some prefer to do it all themselves. Others hire agents to help with the paperwork. In either case, be prepared to answer any questions that may arise during interviews.

-

What should I do after I have found my tenant? If you have a current lease in place you'll need inform your tenant about changes, such moving dates. You can negotiate details such as the deposit and length of stay. Keep in mind that you will still be responsible for paying utilities and other costs once your tenancy ends.

-

How do you collect rent? When it comes to collecting the rent, you will need to confirm that the tenant has made their payments. If not, you'll need to remind them of their obligations. You can subtract any outstanding rent payments before sending them a final check. If you're having difficulty getting hold of your tenant you can always call police. If there is a breach of contract they won't usually evict the tenant, but they can issue an arrest warrant.

-

What can I do to avoid problems? Renting out your house can make you a lot of money, but it's also important to stay safe. Consider installing security cameras and smoke alarms. It is important to check that your neighbors allow you leave your property unlocked at nights and that you have sufficient insurance. You should never allow strangers into your home, no matter how they claim to be moving in.